Alpha Desk

It was a week marked by deep underlying stock dispersion, climbing global yields, and tactical industry rotations as markets balanced escalating rate worries against highly anticipated corporate earnings figures. While major U.S. indexes ground higher, powered by defensive energy flows following the conclusion of the Iran ceasefire,international equities like Europe and South Korea faced substantial distribution. The overarching market narrative points to an environment built for active stock pickers, just as Wall Street prepares for a heavy calendar of inflation data and Q2 banking earnings.

Macro Catalysts: Global Yields Climb as Rate Pressures Mount

The macroeconomic picture shifted hawkishly over the course of the week, putting significant upward pressure on the sovereign debt markets.

Fixed Income Markets Adjust Upward

Sovereign bond yields trended strictly higher across almost every major economic layout, with the exception of Japan and China. U.S. and European paper led the selloff.

Central Bank Expectations Harden

This persistent upward pressure on yields comes as fixed-income desks solidify their projections for monetary policy. Federal Funds Rate (FFR) pricing demonstrates that a formal 25-basis-point rate hike remains firmly expected by the market. While rate-hiking cycles historically pressure broad equity valuations, historical analysis from Goldman Sachs reveals that the S&P 500 typically undergoes its steepest struggles directly at the exact onset of a Fed hiking cycle before gradually stabilizing over a multi-month window.

Equity Action: Extreme Sector & Industry Dispersion

Underneath the surface of a relatively stable U.S. index picture, extreme structural dispersion remained the dominant story of the trading week.

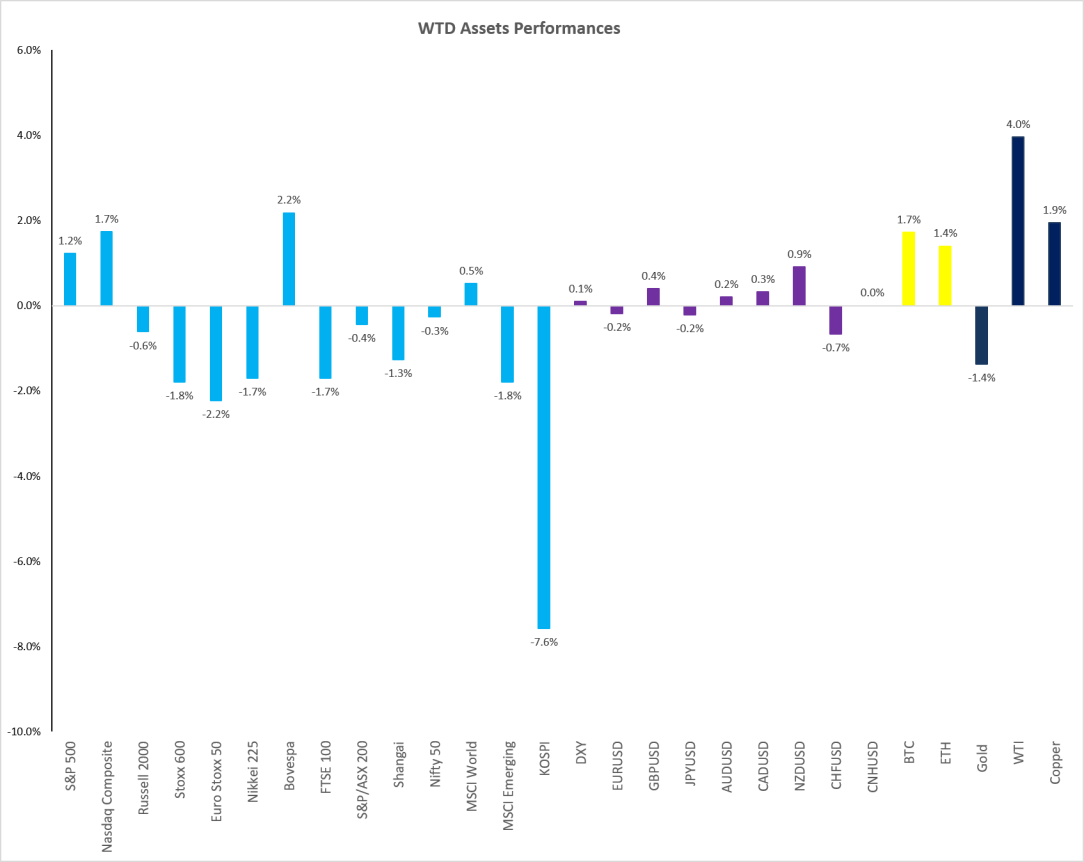

Cross-Asset Snapshot

Major indices diverged sharply based on geographical exposure and tech concentrations:

- U.S. Benchmarks: The Nasdaq Composite led the upside with a +1.7% advance, followed by the S&P 500 at +1.2%. Small caps underperformed, with the Russell 2000 down -0.6%.

- Global Distribution: In stark contrast to previous weeks, Europe showed notable weakness, with the Euro Stoxx 50 falling -2.2%. Emerging markets faced even heavier selling pressure, anchored by a -7.6% drop in South Korea’s KOSPI.

- Commodities & Crypto: Cryptocurrencies remained largely flat, with Bitcoin (BTC) hovering around +1.7% and Ethereum (ETH) at +1.4%. Commodities saw a powerful bid, led by WTI crude oil soaring +4.0% and Copper advancing +1.9%.

Sector & Industry Performance

Sector performance was defined by a massive surge in Energy (+3.5%), which found clear momentum as the ceasefire with Iran officially drew to a close. Information Technology (+2.9%) and Telecommunications (+1.9%) anchored the growth trade, while cyclicals underperformed—evidenced by sharp drops in Materials (-2.1%) and Health Care (-1.8%).

On a granular industry level, dispersion reached extreme limits. Digital Infrastructure (+5.8%) and Oil Services (+5.8%) sat firmly at the top of the leaderboard. Conversely, Aerospace and Defense collapsed -5.6% on a weekly basis, alongside steep drawdowns in Gold Miners (-3.7%) and Homebuilders (-3.5%).

Technical Charts & The Volatility Environment

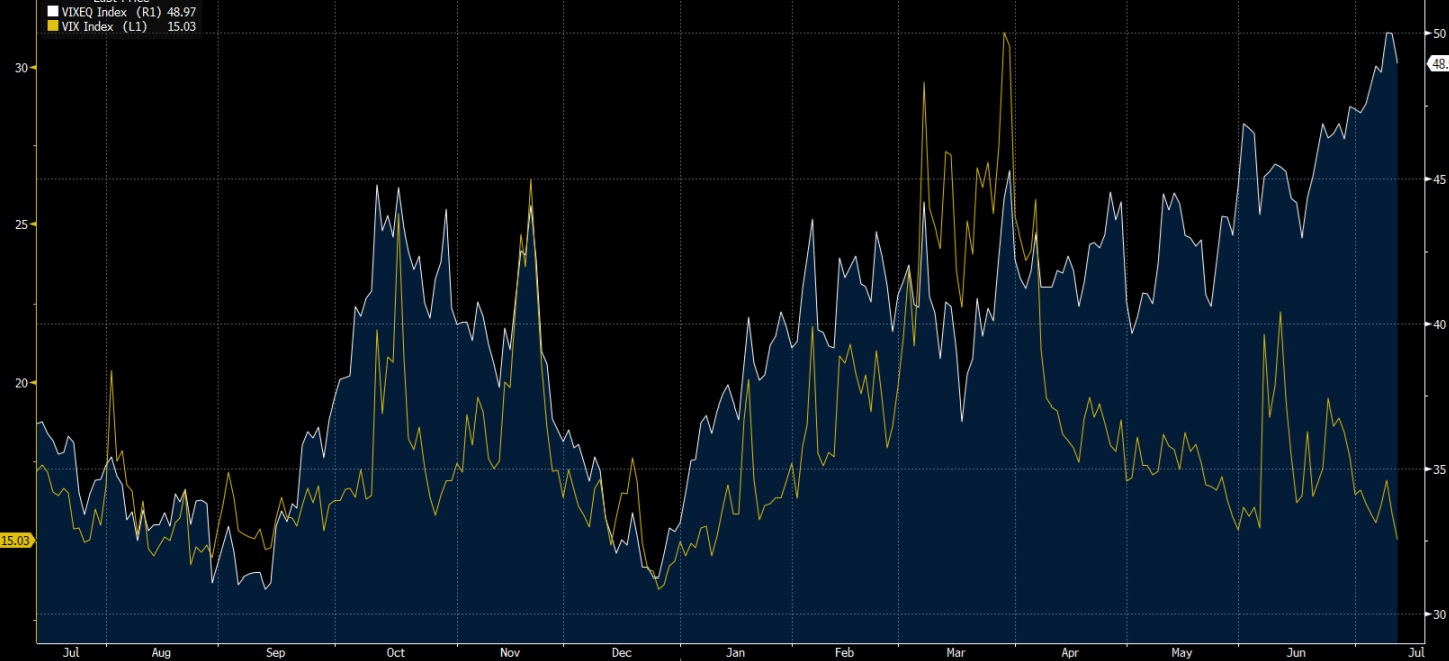

Volatility Back to Baseline

Despite sharp individual stock dispersion, the broad CBOE Volatility Index (VIX) compressed significantly, sliding back down to 15.03%. This marks a complete return to its calm January baselines. However, the pairing of a low VIX alongside a rapidly rising Volatility of VIX (VVIX) index confirms that this has truly evolved into a stock picker’s paradise, where tracking individual names yields far greater alpha than generic macro index positioning.

Technical Analysis Studies

- S&P 500 E-mini Futures (ES): The 5-day volume profile displays an incredibly orderly structural advance. The index successfully carved out a baseline above the heavy volume node, steadily rallying into Friday’s close to settle near 7,626.

- Nasdaq Consolidation: While the broad S&P continues its structural climb, the Nasdaq has entered a well-defined consolidation channel. It remains coiled within a multi-week technical flag pattern, awaiting its next major fundamental catalyst.

The Corporate Health Check: Q2 Earnings Preview

High Growth Hurdles

Corporate America faces exceptionally high bars as the Q2 earnings calendar officially gets underway. Consensus metrics from LSEG I/B/E/S show that the S&P 500 is expected to deliver a massive +23.7% YoY blended earnings growth rate and a strong +11.7% YoY revenue growth print. Growth is anticipated to be overwhelmingly spearheaded by the Technology sector, which is projected to see a staggering +65.5% earnings spike and +33.9% revenue lift.

The Consumer Health Warning

Despite high top-line index expectations, corporate commentary is already flashing cautionary warning signs regarding the core U.S. consumer. On its quarterly earnings call, consumer giant PepsiCo (PEP) issued direct, sobering remarks:

“The consumer is worse than what we had anticipated, and it’s driven mainly by gas prices.”

“However, results were tempered in the quarter as U.S. food and beverage category performance moderated with consumer budgets tightening due to rising inflationary pressures.”

The Week Ahead: CPI Data, Central Bank Speeches, and Banking Earnings

The incoming calendar shifts immediately into high gear, introducing multi-layered risk events via high-impact economic data, non-stop Federal Reserve commentary, and critical financial sector prints.

High-Impact Macro Calendar

- 13-Jul (Monday): Federal Budget Balance.

- 14-Jul (Tuesday): Consumer Price Index (CPI); Real Average Weekly Earnings; TIC Flows; NFIB Small Business Optimism.

- 15-Jul (Wednesday): Empire State Manufacturing; Producer Price Index (PPI); Fed Releases Beige Book.

- 16-Jul (Thursday): Retail Sales; Business Inventories; NAHB Housing Market Index.

- 17-Jul (Friday): Housing Starts; Building Permits; Global Trade Data; University of Michigan Consumer Sentiment.

Fed Speakers: Pre-Blackout Blitz

Fixed income and currency desks will have to navigate a remarkably dense schedule of central bank communications as Fed officials hit the tape heavily right before entering their official pre-meeting communications blackout window:

- Monday: Bowman (Financial Regulation) and Waller (NYABE).

- Tuesday: Fed Chair Warsh testifies before the House Financial Services Committee; Barr (AI discussion), Goolsbee, Cook, and Bowman speak later in the session.

- Wednesday: Williams delivers keynote remarks; Fed Chair Warsh testifies before the Senate Banking Committee; Cook speaks on the economic outlook.

- Thursday: Logan addresses economy/monetary policy; Schmid speaks at the Kansas City Fed Forum.

- Friday: Jefferson speaks on monetary policy before the midnight communications blackout begins.

Major Banking & Corporate Earnings

The corporate world formally kicks off its Q2 reporting season, with major Wall Street banking institutions dominating the early tape:

- Tuesday: Citigroup (C), JPMorgan Chase (JPM), State Street (STT), Wells Fargo (WFC), Fastenal (FAST), Ericsson (ERIC).

- Wednesday: ASML Holding (ASML), Progressive (PGR), BlackRock (BLK), Morgan Stanley (MS), United Airlines (UAL), PNC Financial (PNC).

- Thursday: Taiwan Semiconductor Manufacturing Co. (TSMC), Netflix (NFLX), US Bancorp (USB), Blackstone (BX), Abbott Laboratories (ABT), Alcoa (AA).

- Friday: Regions Financial (RF), Truist Financial (TFC), American Express (AXP), Travelers (TRV), Autoliv (ALV).

Trader’s Note: Treasury auction supply is muted this week, focusing primarily on short-duration Bills. Meanwhile, the SPY Weekly Straddle is pricing an exceptionally tight implied move of just +/- 1.1%. With highly compressed index optionality colliding directly with a critical CPI release and major money-center banking earnings, current premium levels offer defensive macro traders an attractive opportunity to secure cross-asset protection.

Stay Connected

Want to dive deeper or join the community?

📧 Book mentoring for Q3 2026: https://duponttrading.com/mentoring/

🎥 Access the 4×4 video series: https://duponttrading.com/4×4-course/

💬 Join the Discord: 30 channels of trading insights: https://discord.com/invite/Yf42SgAx7f

https://buy.stripe.com/5kA3dmdVV1g4cuIaEE

For any questions or to join our mentoring sessions, email us at Greg📩Contact: greg@duponttrading.com

Have a good Trading Week!

Sub Section Title Here

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

THIS POST

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

ACCESS FREE LECTURESUBSCRIBE

TO OUR BLOG

To receive opinions, market research, and data analysis in the Financial Markets

ABOUT

DUPONT TRADING

As a Professional Trader/Portfolio Manager/Hedge Fund Manager for almost 20 years, I know that learning how to Trade/Invest is a non-ending learning curve. This adventure is extremely exciting but needs to be ridden carefully.

In January 2018 after receiving many requests, I decided to start my own mentoring activities.

In October 2019, I launched the 4×4 Video Series to help Investors profitably manage their portfolios. By sharing my ideas/experiences and offering education through the 4×4 Video Series, I hope I can help you becoming a better investor.

Students

Testimonials

K. (United Kingdom)

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.