Macro Horizon

It was a striking week of tactical shifts on Wall Street and across global exchanges. While a highly anticipated macroeconomic dataset presented a mixed picture highlighted by a cooling global manufacturing expansion and a surprisingly soft jobs print—equity markets staged a definitive rotation. The prevailing narrative centered around a risk-on wave triggered by a less-hawkish-than-feared Federal Reserve tone, sparking a notable unwind in high-beta momentum and fueling a structural breakout in European indices.

Macro Catalysts: Rising Yields vs. Soft Jobs Data

The fundamental macroeconomic indicators continuing to roll in presented conflicting signals, yet ultimately provided equity bulls with a green light as monetary pressures eased.

Yields Edge Upwards but USD Softens

Sovereign debt yields experienced upward pressure across most major global economies. However, because former Fed Governor Kevin Warsh struck a less hawkish tone than institutional desks anticipated, the U.S. Dollar (DXY) weakened, fostering an environment favorable to global risk assets. Yield movements detailed a general shift higher.

Central Bank Policy Trajectory

Fixed-income futures markets are reacting closely to these adjustments. The Federal Funds Rate (FFR) futures curve indicates that the market is now actively pricing in a 25 basis point rate hike for late 2026. The effective rate sits at 3.63% against a 3.75% target rate, with structural expectations drifting slightly more aggressive out to late 2027 before flattening.

Cool Global PMIs and Soft Payrolls

On the broader macroeconomic front, the ISM and manufacturing PMI data printed at acceptable baseline levels. The Global PMI cooled slightly, coming down from 52.7 to 52.2.

Concurrently, labor market pressures eased significantly. The Non-Farm Payrolls (NFP) print came in substantially lower than consensus estimates at just 57k, marking a steep cooldown from prior months.

The AI Trade Reverses as Value Bids Up

Despite a structurally positive macro backdrop, thematic equity shifts took center stage as high-flying momentum trades experienced sharp profit-taking.

The Momentum Unwind

High-beta momentum names faced severe selling pressure on a weekly basis, as evidenced by a comprehensive factor breakdown. The top downside themes included:

- High Beta Momentum: -11.63%

- Bitcoin Sensitive: -14.64%

- Momentum Long / Short Momentum: -9.56%

- AI Datacenter Electrification Beneficiaries: -4.81%

This clean-out was partly driven by corporate commentary, notably from Meta (META), indicating they could begin utilizing over-capacity for their cloud business. This triggered an immediate, sharp weekly reversal in the AI trade, with semiconductors getting hit hard while previously unloved software names caught a powerful defensive bid.

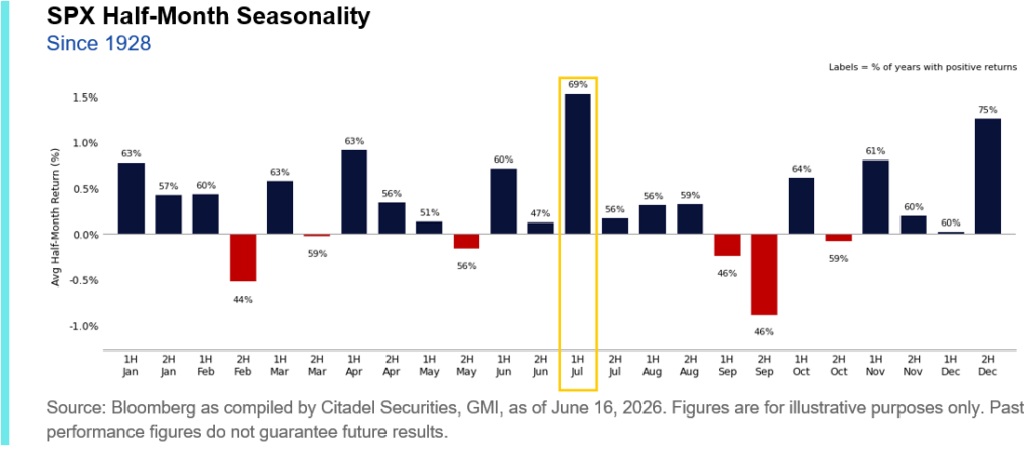

The July Seasonal Anomaly

This rotation aligns with an underappreciated historical pattern. While July is typically recognized as a strongly positive calendar month for the broad S&P 500, a historical 10-year tracking grid reveals it has historically been an exceptionally difficult month for the pure momentum factor, frequently generating deeply negative factor returns.

Asset Class and Sector Performance

Cross-Asset Snapshot

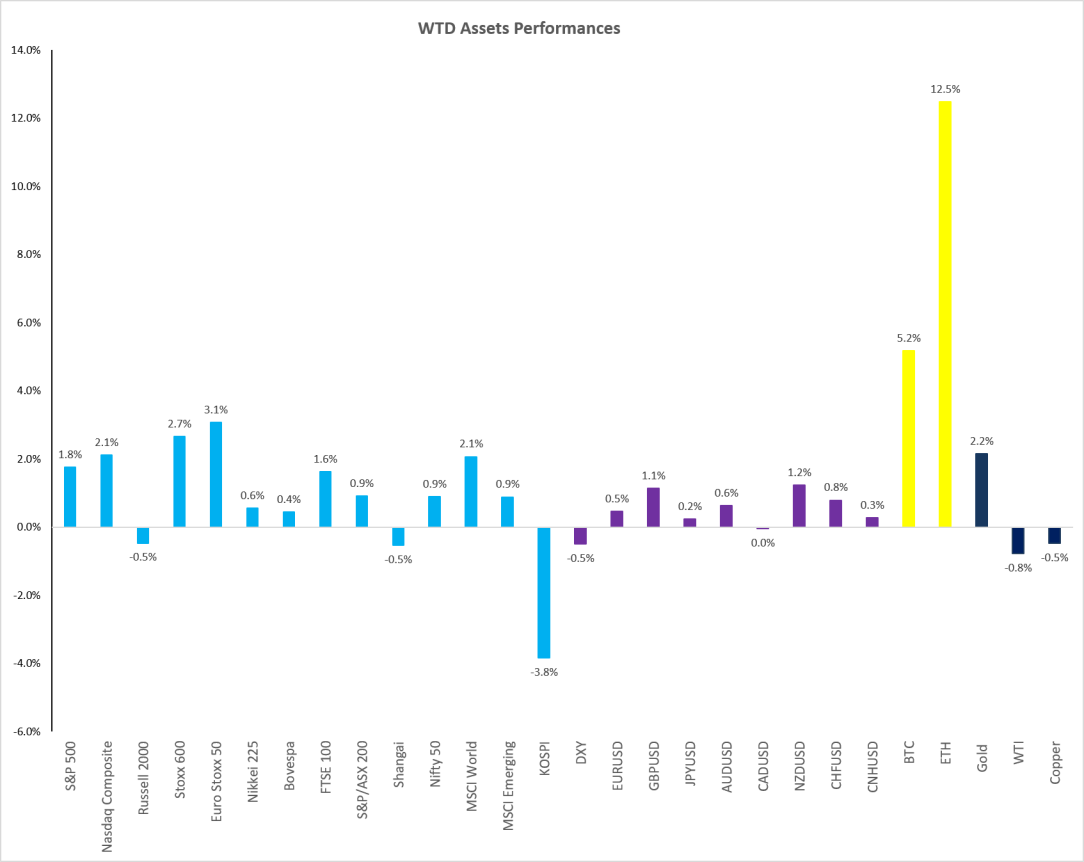

Broad indices were generally resilient, though localized pockets of momentum underperformed:

- U.S. Indices: The S&P 500 rose +1.8% and the Nasdaq Composite climbed +2.3%. The small-cap Russell 2000 underperformed slightly on a weekly basis, down -0.5%.

- Global Outperformance: The Euro Stoxx 50 rallied a strong +3.3%. Conversely, high-momentum global markets like South Korea’s KOSPI dropped -3.8% as risk-on capital rotated elsewhere.

- Commodities & Crypto: Cryptocurrencies staged a powerful bounce, with Bitcoin (BTC) gaining +5.2% and Ethereum (ETH) surging +12.5%. WTI crude oil declined -0.8%, bringing welcome relief to global industrial inputs.

Sector & Industry Breakdown

The sector charts highlighted a definitive tilt toward cyclicals and value pockets. Financially strong industries led the charge as yields trended higher, with Financials gaining +5.8% on the week, followed closely by Telecommunications (+3.2%) and Consumer Discretionary (+2.4%). Information Technology experienced minor distribution, sliding -0.4%.

On an industry basis, Cyber Security, Software, and Social Media paced the weekly leaderboard. Meanwhile, Digital Infrastructure, Oil Services, and Semiconductors sat firmly at the bottom of the weekly performance ladder, undergoing a major positioning reset.

Volatility Reset & Technical Charts

Volatility Compresses

Following the tactical factor shifts, risk premium saw an orderly compression. The CBOE Volatility Index (VIX) settled comfortably below the 16% threshold, closing the week at 15.81%, reflecting a healthy systemic pullback.

Technical Chart Studies

- S&P 500 E-mini Futures (ES): The 5-day volume profile chart highlights an incredibly robust equity structure. Market price action successfully reclaimed and defended the vital 7,550 level, building a structural baseline for higher targets.

- European Breakout (German DAX): Driven by a combination of domestic German stimulus measures, lower crude oil inputs, and the powerful systemic rotation out of momentum and into value, the German DAX broke out comprehensively to score new all-time highs.

- The Robotics Theme: Institutional interest continues to expand rapidly within the robotics and automation space. European industrials (across Sweden, Germany, and France) alongside Japanese engineering firms are emerging as primary structural beneficiaries of this expanding capital allocation trend.

Earnings Revisions and Valuation Multipliers

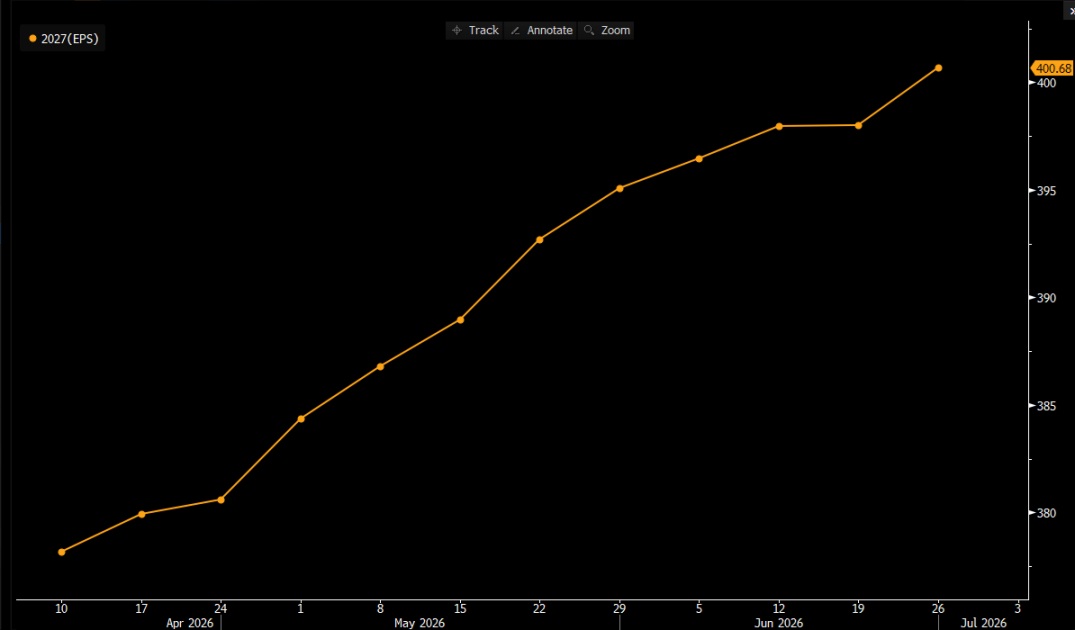

Forward EPS Trends

The near-term corporate backdrop shows a divergence across calendar years. Consensus expectations for Q2 2026 and full-year 2026 EPS have started to look somewhat toppish, flattening out over the final weeks of June.

However, forward revisions for 2027 EPS keep steadily climbing, recently accelerating toward $400.68. Utilizing standard institutional multiplier blocks against this projected $400 base yields the following structural targets for the S&P 500 index:

- $400 x 20 = 8,000

- $400 x 21 = 8,400

- $400 x 22 = 8,800

Valuation Context

This calculation aligns closely with current historical multiples. As tracked below, the S&P 500 Forward P/E ratio currently registers at 20.4x. While this sits above the long-term 30-year average of 17.2x, it remains perfectly bounded near the +1 standard deviation line (20.5x), suggesting valuations are full but fundamentally supported by rising outer-year earnings power.

Source: J.P. Morgan

The Week Ahead: ISM Services and FOMC Minutes

The macroeconomic calendar shifts focus heavily toward secondary labor datasets, service sector health, and central bank transcript releases.

High-Impact Macro Calendar

- 06-Jul (Monday): ISM Services Index.

- 07-Jul (Tuesday): ADP Weekly Employment Change; Global Trade Balance.

- 08-Jul (Wednesday): Wholesale Inventories; FOMC Meeting Minutes; Consumer Credit.

- 09-Jul (Thursday): Existing Home Sales.

Central Bank Speakers and Auctions

Fixed-income markets will have to digest a dense schedule of official central bank commentary and major Treasury supply auctions:

- Monday: Fed’s Waller alongside the ECB’s Schnabel, Wunsch, and Riksbank’s Seim live in Rome.

- Wednesday: Publication of the FOMC June Meeting Minutes.

- Thursday: Fed’s Williams in a moderated discussion panel.

- Thursday: Fed’s Logan moderates an institutional panel on Market Liquidity.

- Treasury Auctions: Desk liquidity will be tested via consecutive multi-billion dollar offerings, featuring 3-Year notes on Tuesday, 9-Month to 10-Month notes on Wednesday, and 29-Year to 10-Month bonds on Thursday.

Corporate Earnings Pipeline

The corporate earnings calendar remains seasonally light as the market prepares for the formal kickoff of the Q2 cycle by major money-center banking institutions in mid-July. Key names reporting include:

- Tuesday: Penguin Solutions (PENG), Enerpac Tool Group (EPAC), Kura Sushi (KRUS)

- Wednesday: Helen of Troy (HELE), Levi Strauss & Co. (LEVI), AZZ Inc. (AZZ)

- Thursday: PepsiCo (PEP), WD-40 Company (WDFC), Simply Good Foods (SMPL)

- Friday: Delta Air Lines (DAL)

Trader’s Note: The SPY Weekly Straddle is currently pricing an implied move of +/- 1.3%. Given the significant compression in the VIX, a massive schedule of high-volume Treasury auctions, and the formal parsing of the FOMC minutes, short-dated index optionality is offering attractive relative value for defensive hedging. Keep risk parameters strictly defined.

Stay Connected

Want to dive deeper or join the community?

📧 Book mentoring for Q3 2026: https://duponttrading.com/mentoring/

🎥 Access the 4×4 video series: https://duponttrading.com/4×4-course/

💬 Join the Discord: 30 channels of trading insights: https://discord.com/invite/Yf42SgAx7f

https://buy.stripe.com/5kA3dmdVV1g4cuIaEE

For any questions or to join our mentoring sessions, email us at Greg📩Contact: greg@duponttrading.com

Have a good Trading Week!

Sub Section Title Here

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

Related Articles

The Structural Edge

It was a week of stark cross-asset dispersion on Wall Street. While macroeconomic…

VIEW POST

Rockets, Rotation, and Relief: How SpaceX and Cool CPI Fueled a Small-Cap Surge

Early-week liquidation fears evaporated as a historic $2.2T SpaceX debut, a soft Core…

VIEW POSTTHIS POST

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

ACCESS FREE LECTURESUBSCRIBE

TO OUR BLOG

To receive opinions, market research, and data analysis in the Financial Markets

ABOUT

DUPONT TRADING

As a Professional Trader/Portfolio Manager/Hedge Fund Manager for almost 20 years, I know that learning how to Trade/Invest is a non-ending learning curve. This adventure is extremely exciting but needs to be ridden carefully.

In January 2018 after receiving many requests, I decided to start my own mentoring activities.

In October 2019, I launched the 4×4 Video Series to help Investors profitably manage their portfolios. By sharing my ideas/experiences and offering education through the 4×4 Video Series, I hope I can help you becoming a better investor.

Students

Testimonials

K. (United Kingdom)

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.