The Structural Edge

It was a week of stark cross-asset dispersion on Wall Street. While macroeconomic data offered a supportive backdrop—characterized by cooling energy markets and a well-received PCE inflation print—equity markets faced internal plumbing pressures. The core narrative centered around a growing institutional skepticism toward relentless artificial intelligence infrastructure spend, leaving mega-cap tech on the defensive even as underlying fixed-income volatility reset.

Macro Catalysts: Lower Oil and Stable PCE Drag Yields Down

The fundamental macro data continuing to roll in has given global central banks clear breathing room, helping push sovereign yields lower across major global economies.

Global Yield Curve Retracts

Sovereign debt caught a strong bid this week, primarily driven by a downward flush in WTI crude oil prices—which broke below the $70 handle—alongside an “in-line” PCE deflator print. Global 10-year yields fell across the board:

The long-term trajectory of the United States 10-Year Treasury note remains bounded within its multi-year structural channel following its late-2023 peak.

Monetary Policy Horizons

Fixed-income futures markets are currently pricing a highly stable outlook for the Federal Reserve. The market is effectively projecting exactly one interest rate hike over the remaining horizon of the year, tracking an effective Federal Funds Rate of 3.63% against a 3.75% target rate.

Mega-Cap Tech Faces a Capex Reckoning

Despite spectacular micro-level fundamental execution within the technology supply chain, structural factor rotations dominated equity markets.

The Micron Conundrum

Micron Technology (MU) dropped an absolute blockbuster Q3 earnings report:

- Q3 Revenue: $41.5 billion vs. $35.9 billion FactSet consensus.

- Q3 EPS: $24.67 per share.

- Q4 Outlook: Projected revenue of $49.0–51.0 billion easily clearing the $43.6 billion consensus mark, alongside a staggering expected 86% gross margin.

Yet, this was still not enough to hold up the broader market. The Magnificent 7 and global hyperscalers shed -5% on the week and are now trading lower by -12% over the trailing month. Institutional desks are increasingly penalizing massive capital expenditure (capex) budgets allocated to AI infrastructure, noting that the immediate trade-off has been a significant reduction in near-term free cash flow (FCF) margins and share buyback programs.

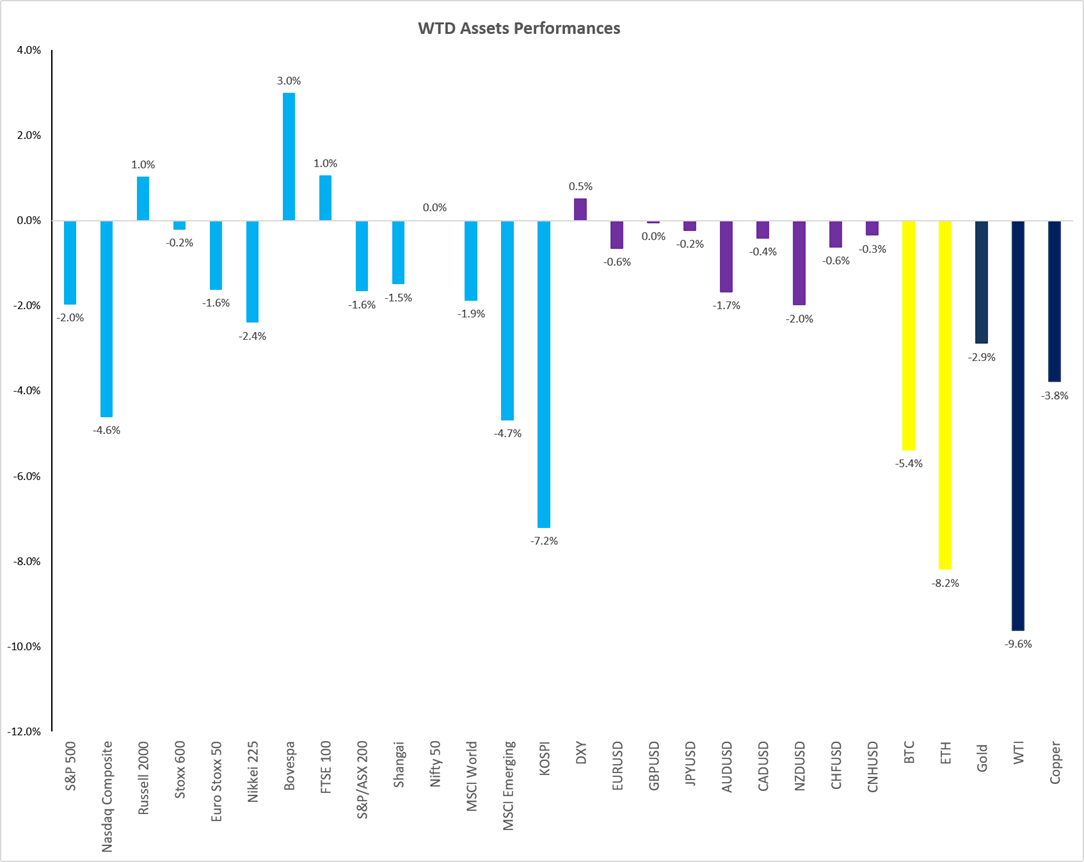

Asset Class and Factor Performance

Broad Market De-risking

The thematic execution across global macro spaces was distinctively risk-off. Large caps drifted while crypto networks bore the brunt of liquidity contractions:

- Large Caps vs. Small Caps: The Nasdaq Composite shed -4.6% and the S&P 500 gave up -2.0%. Conversely, the Russell 2000 notched a +1.0% weekly gain, continuing its clear relative outperformance.

- International Flushes: South Korea’s KOSPI index plunged -7.2% on the week.

- Commodities Check: WTI Crude collapsed -9.6% to slide below $70, while Gold retraced -2.9%.

- Crypto Meltdown: Bitcoin (BTC) dropped -5.8% to trade near the key $60k psychological support line, while Ethereum (ETH) lost -8.2%.

Sector & Industry Breakdown

Defensive sectors acted as the ultimate hiding places on the week. Health Care surged a powerful +7.8%, while Real Estate (+4.1%) and Utilities (+3.9%) handily beat the broader S&P 500’s -2.4% sector drop.

On an industry basis, Semiconductors continue to maintain their title as the premier Year-to-Date structural winner despite enduring massive profit-taking and distribution on a weekly basis. Silver, Nuclear, and Metals & Mining sat at the absolute bottom of the weekly performance ladder.

Volatility Reset & Market Technicals

The Volatility Equation

Following a comprehensive post-OpEx flush, the market experienced a healthy clean-out of short-dated premium. The CBOE Volatility Index (VIX) settled the week at 18.41%. This level represents a normal cyclical mean-reversion within the wider structural baseline observed since 2022.

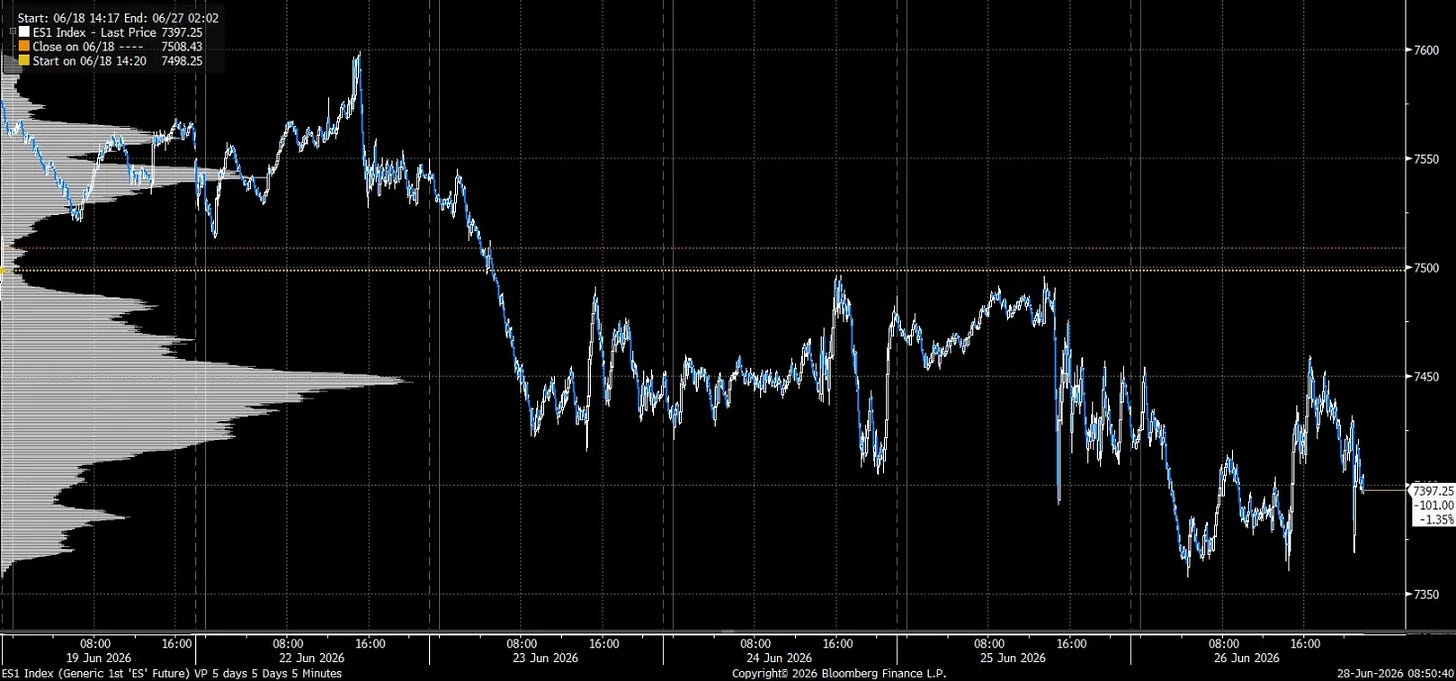

Technical Chart Studies

- S&P 500 E-mini Futures (ES): The 6-day volume profile view in details a market consolidating down into immediate structural value blocks, closing near 7,397.25. The longer-term weekly trend demonstrates that the baseline secular ascending channel remains flawlessly intact.

- Nasdaq Composite: Shows similar consolidative properties but with significantly wider historical beta and localized volatility.

- USD/JPY: Remains one of the critical macro charts to monitor globally as it coils inside an extremely tight multi-month technical wedge boundary.

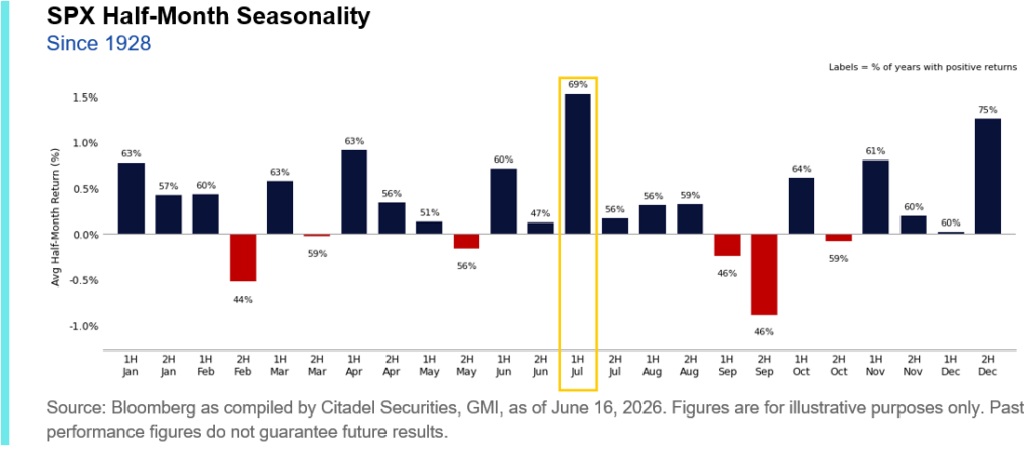

Seasonality and Forward Earnings Expectations

The July Seasonality Tailwind

While the final leg of June trading historically presents structural positioning friction, historical tendencies indicate a potent near-term shift. According to 20-year S&P 500 seasonal analytics, market performance heavily inflects positive entering the summer months.

More granularly, the SPX Half-Month Seasonality dataset compiled by Citadel Securities since 1928 shows that the first half of July ranks as one of the single most reliably bullish two-week periods of the entire calendar year, sporting positive historical returns in 69% of recorded years.

Q2 Earnings Outlook

The forward-looking fundamental catalyst arrives via the Q2 corporate reporting cycle kicking off in mid-July.

Forward aggregate EPS estimates have remained relatively flat over the last month with an absence of fresh upward revisions. However, the overarching baseline has seen a tremendous expansion since the start of the year. Aggregate S&P 500 Q2 earnings growth is currently projected to land at a stellar +24.3% YoY, fueled predominantly by massive expansions in Energy (+118.0%) and Technology (+65.4%).

The Week Ahead: Non-Farm Payrolls and Central Bank Forums

The upcoming economic docket is uniquely compressed due to the U.S. market closure on Friday, July 3rd. Consequently, the vital monthly Non-Farm Payroll (NFP) print will drop on Thursday morning instead, making it a highly volatile pre-holiday session.

High-Impact Macro Calendar

- 29-Jun (Monday): Dallas Fed Manufacturing Activity.

- 30-Jun (Tuesday): FHFA House Price Index; JOLTs Job Openings; Conference Board Consumer Confidence.

- 01-Jul (Wednesday): Challenger Job Cuts; ADP Employment Change; ISM Manufacturing PMI; Construction Spending.

- 02-Jul (Thursday): Change in Non-Farm Payrolls (NFP); Unemployment Rate; Factory Orders; Durable Goods Orders.

- 03-Jul (Friday): U.S. Markets Closed (Independence Day Observed).

Central Bank Speakers Spotlight

The global central banking elite will be highly active, congregating at the ECB Forum on Central Banking:

- Sunday: Fed’s Barkin at Aspen Ideas Panel.

- Wednesday: Joint ECB Panel featuring Lagarde, Fed’s Warsh, BOE’s Bailey, and BOC’s Macklem.

- Wednesday: Fed’s Warsh appears individually on an ECB Forum panel.

- Thursday: Fed’s Daly speaks in a moderated conversation.

Q2 Earnings On Deck

The corporate reporting calendar is light but carries immense consumer and tech-adjacent significance:

- Monday: AeroVironment (AVAV), Concentrix (CNXC)

- Tuesday: Nike (NKE), Progress Software (PRGS)

- Wednesday: General Mills (GIS), MSC Industrial (MSM)

- Thursday: Lindsay Corporation (LNN)

Trader’s Note: The SPY Weekly Straddle is currently pricing an implied move of +/- 1.6%. Given the compressed 4-day trading week, the clustering of central bank forum headlines, and the shift of the NFP print to Thursday morning, volatility is severely underpricing potential tail risk. Ensure your risk controls are absolute heading into the long weekend.

Stay Connected

Want to dive deeper or join the community?

📧 Book mentoring for Q3 2026: https://duponttrading.com/mentoring/

🎥 Access the 4×4 video series: https://duponttrading.com/4×4-course/

💬 Join the Discord: 30 channels of trading insights: https://discord.com/invite/Yf42SgAx7f

https://buy.stripe.com/5kA3dmdVV1g4cuIaEE

For any questions or to join our mentoring sessions, email us at Greg📩Contact: greg@duponttrading.com

Have a good Trading Week!

Sub Section Title Here

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.

Related Articles

Rockets, Rotation, and Relief: How SpaceX and Cool CPI Fueled a Small-Cap Surge

Early-week liquidation fears evaporated as a historic $2.2T SpaceX debut, a soft Core…

VIEW POST

The Great Volatility Awakening

A violent risk-off reversal shatters thin-volume all-time highs as hawkish Fed pricing, a…

VIEW POSTTHIS POST

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.

ACCESS FREE LECTURESUBSCRIBE

TO OUR BLOG

To receive opinions, market research, and data analysis in the Financial Markets

ABOUT

DUPONT TRADING

As a Professional Trader/Portfolio Manager/Hedge Fund Manager for almost 20 years, I know that learning how to Trade/Invest is a non-ending learning curve. This adventure is extremely exciting but needs to be ridden carefully.

In January 2018 after receiving many requests, I decided to start my own mentoring activities.

In October 2019, I launched the 4×4 Video Series to help Investors profitably manage their portfolios. By sharing my ideas/experiences and offering education through the 4×4 Video Series, I hope I can help you becoming a better investor.

Students

Testimonials

K. (United Kingdom)

LEARN ONLINE TRADING TODAY. THE PROFESSIONAL WAY.

Let us solve the problem and confusion around trading and finance management, the right way.